These Were The Largest Sovereign Debt Defaults In Modern History

Who´s next? (Hint: the government which has over $35 trillion in debts they cannot pay.)

These Were The Largest Sovereign Debt Defaults In Modern History

BY TYLER DURDEN

SATURDAY, AUG 17, 2024

In July, Ukraine avoided defaulting on $20 billion in loans by reaching a preliminary agreement with private creditors.

Given the financial burden of war, the country suspended interest payments on international debt over the last two years, which was set to expire on August 1, 2024.

Without this new debt restructuring, this default would have ranked among the 10 largest in recent history. The last time Ukraine defaulted on its debt was in 2015, after Russia’s invasion of Crimea.

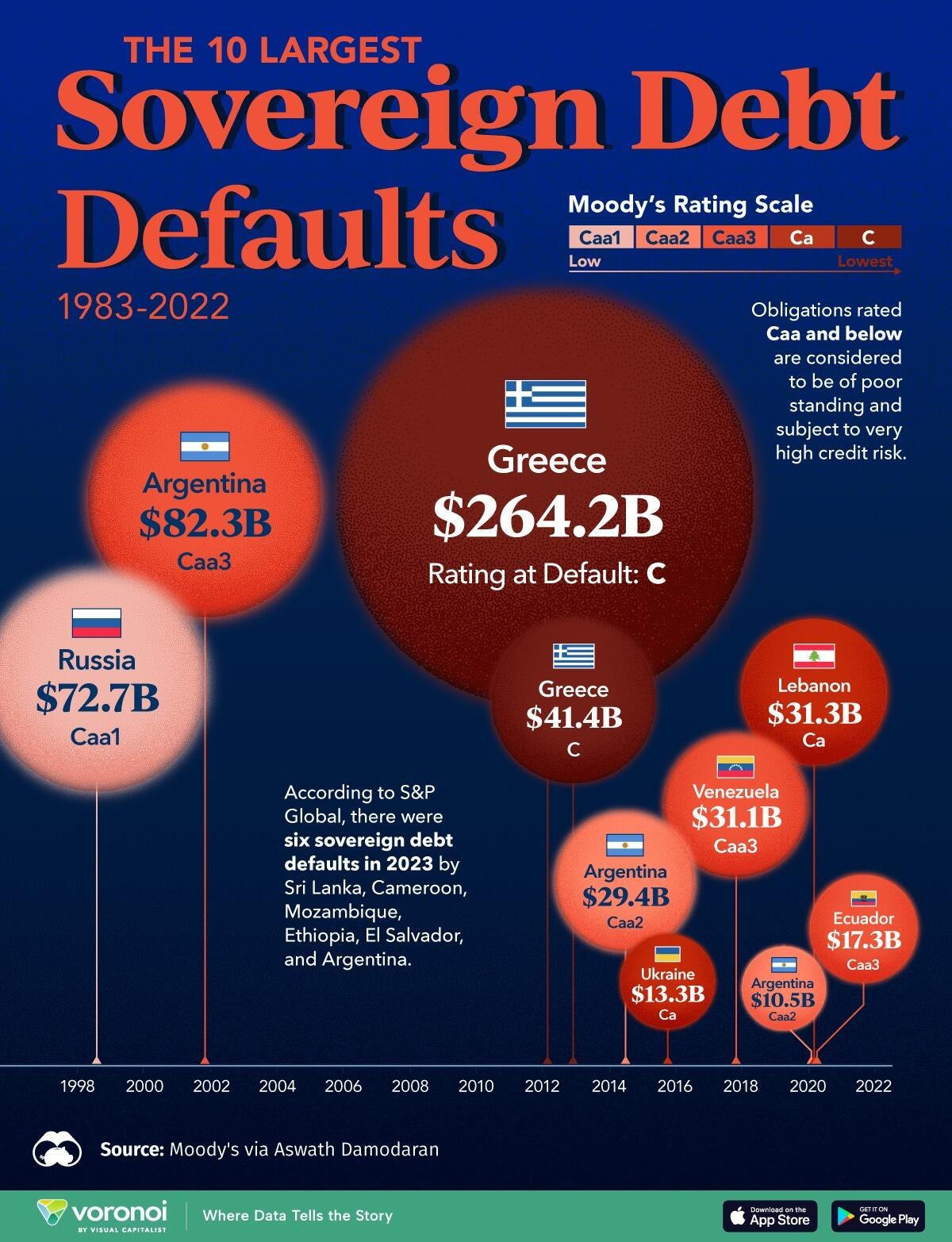

This graphic, via Visual Capitalist's Dorothy Neufeld, shows the largest sovereign debt defaults since 1983, based on data from Moody’s via Aswath Damodaran.

The Top 10 Sovereign Debt Defaults

Below, we show the biggest sovereign debt defaults between 1983 and 2022:

Greece’s $264.2 billion default in 2012 stands as the largest overall, unfolding when the country was mired in recession for the fifth consecutive year.

The country defaulted again just nine months later, making it the fourth-largest ever. Leading up to the crash, Greece ran significant deficits despite being one of the fastest-growing countries in Europe. Furthermore, in 2009, the newly elected prime minister revealed that the country was $410 billion in debt—substantially more than previous estimates.

With the second-highest default recorded, Argentina failed to repay interest on $82.3 billion in foreign debt in 2001. Like Greece, it is a repeat offender, defaulting numerous times since independence in 1816. Today, Argentina is the largest debtor to the International Monetary Fund, despite being Latin America’s third-largest economy.

Following next in line is Russia’s 1998 default on $72.7 billion in loans, coinciding with a currency crisis that erased more than two-thirds of the ruble’s value in a matter of weeks. That year, several other countries including Venezuela, Pakistan, and Ukraine defaulted on their debts after the Asian Financial Crisis of 1997 spurred instability in global financial markets.

Just as 1998 saw a wave of defaults, 2020 was a year marked by major debt upheavals. Due to the pandemic and collapsing oil prices, it was a record year for sovereign defaults, reaching seven in total. Among these, Lebanon, Ecuador, and Argentina saw the largest defaults amid deepening fiscal pressures.

https://www.zerohedge.com/geopolitical/these-were-largest-sovereign-debt-defaults-modern-history

/////

Credit downgrades of countries have increased in 11 of the past 12 years.

For more details, charts, etc. read more at

https://www.spglobal.com/ratings/en/research/articles/210412-default-transition-and-recovery-2020-annual-sovereign-default-and-rating-transition-study-11888070

Default, Transition, and Recovery: 2020 Annual Sovereign Default And Rating Transition Study

Ratings Performance Analytics:Nick W Kraemer, Evan M Gunter, Vincent R Conti

Research Contributors:Abhik Debnath, Lyndon Fernandes

View Analyst Contact Information

Table of Contents

Key Takeaways

Sovereign defaults reached a record high of seven in 2020 as COVID-19 and falling oil prices hurt global credit quality; all the defaulters began the year rated 'B' or lower.

Sovereign downgrades rose to 26, and most were of speculative-grade issuers from the emerging and frontier markets.

Despite the unprecedented economic, social, and financial market turmoil in 2020, sovereign credit ratings showed solid performance with a one-year Gini ratio of 91.5%, near the long-term average.

By the end of 2020, the number of sovereigns rated at the lowest rating levels, 'CCC+' and below, had risen to seven, suggesting defaults could remain elevated in coming years.

The spread of COVID-19 and the collapse of oil prices created challenging credit conditions for sovereigns rated by S&P Global Ratings in 2020. The number of sovereign defaults climbed to a high of seven, while downgrades rose to their highest tally since 2011 and outnumbered upgrades by a ratio of 10 to 1.

With the global economy falling into a sudden recession in the first half of 2020, sovereigns that entered the year with weaker ratings were most exposed. All of the defaults were from sovereigns rated 'B' or lower, and most downgrades were of speculative-grade sovereigns (rated 'BB+' or lower) from the emerging and frontier markets.

In 2021, sovereign ratings may continue to face pressure amid expected massive fiscal and monetary stimulus that will leave a substantial debt overhang for several years to come.

Sovereign Defaults Reached A High In 2020

There were seven sovereign defaults in 2020, marking the highest annual tally on record. Before 2020, the high for defaults was six, in 2017. The defaulters in 2020 entered the year with already weakened credit metrics--none were rated above 'B'--and had little room to absorb the impact of the pandemic-induced recession.

Chart 1

Suriname was the highest-rated sovereign to default in 2020, with a 'B' long-term foreign currency rating at the start of the year. Two of the defaulters (Ecuador and Belize) were rated 'B-' as of the beginning of 2020, and three (Zambia, Lebanon, and Argentina) were rated in the lowest rating category, 'CCC'/'CC'.

All of the defaults in 2020 were from emerging and frontier market sovereigns. By region, Latin America had the most defaults, with five, from Argentina, Belize, Ecuador, and Suriname (which defaulted twice). The other two defaulters, Lebanon and Zambia, were from the Middle East and Africa region.

All but one of these sovereign defaults resulted to some extent from the unprecedented credit challenges of COVID-19 and the oil price collapse. Both Ecuador and Suriname grappled with economic shocks as falling oil prices hit exports. This led Ecuador to delay payment on a number of global bonds in April after reaching agreements with a majority of its respective bondholders. Suriname defaulted twice in 2020: In July it began and completed a distressed debt exchange, and by end-October, the new government proposed a standstill on foreign currency debt service payments.

Meanwhile, Belize faced a sharp economic contraction from the COVID-19 pandemic, and as its tourism industry reeled, the government reached an agreement with bondholders in August to amend the terms on its 2034 bond.

Zambia's access to liquidity and external financing became impaired as investors curtailed their exposure to credit risk in response to the pandemic, and the Zambian government suspended debt service payments to external commercial creditors in October.

In Argentina, the pandemic heightened the fiscal strain of weaker revenue, higher expenditure, and unfavorable conditions in the external financing markets. The sovereign missed payments of local-law U.S. dollar-denominated bonds in April and of foreign-law foreign currency bonds in June.

Only Lebanon's default was unrelated to COVID-19, with the fiscal, external, and political pressures that led to the eventual default preceding COVID-19's impact on the country. Lebanon confirmed its first case of COVID-19 on Feb. 21, 2020, and in an unrelated rating action on the same day, we lowered our long-term foreign currency rating on the country to 'CC' because a distressed exchange or unilateral default was virtually certain.

Charts 2 through 7 show the rating histories of these sovereigns that defaulted in 2020.

read more at

Default, Transition, and Recovery: 2020 Annual Sovereign Default And Rating Transition Study

Ratings Performance Analytics:Nick W Kraemer, Evan M Gunter, Vincent R Conti

Research Contributors:Abhik Debnath, Lyndon Fernandes

View Analyst Contact Information

Table of Contents

Key Takeaways

Sovereign defaults reached a record high of seven in 2020 as COVID-19 and falling oil prices hurt global credit quality; all the defaulters began the year rated 'B' or lower.

Sovereign downgrades rose to 26, and most were of speculative-grade issuers from the emerging and frontier markets.

Despite the unprecedented economic, social, and financial market turmoil in 2020, sovereign credit ratings showed solid performance with a one-year Gini ratio of 91.5%, near the long-term average.

By the end of 2020, the number of sovereigns rated at the lowest rating levels, 'CCC+' and below, had risen to seven, suggesting defaults could remain elevated in coming years.

The spread of COVID-19 and the collapse of oil prices created challenging credit conditions for sovereigns rated by S&P Global Ratings in 2020. The number of sovereign defaults climbed to a high of seven, while downgrades rose to their highest tally since 2011 and outnumbered upgrades by a ratio of 10 to 1.

With the global economy falling into a sudden recession in the first half of 2020, sovereigns that entered the year with weaker ratings were most exposed. All of the defaults were from sovereigns rated 'B' or lower, and most downgrades were of speculative-grade sovereigns (rated 'BB+' or lower) from the emerging and frontier markets.

In 2021, sovereign ratings may continue to face pressure amid expected massive fiscal and monetary stimulus that will leave a substantial debt overhang for several years to come.

Sovereign Defaults Reached A High In 2020

There were seven sovereign defaults in 2020, marking the highest annual tally on record. Before 2020, the high for defaults was six, in 2017. The defaulters in 2020 entered the year with already weakened credit metrics--none were rated above 'B'--and had little room to absorb the impact of the pandemic-induced recession.

Chart 1

Suriname was the highest-rated sovereign to default in 2020, with a 'B' long-term foreign currency rating at the start of the year. Two of the defaulters (Ecuador and Belize) were rated 'B-' as of the beginning of 2020, and three (Zambia, Lebanon, and Argentina) were rated in the lowest rating category, 'CCC'/'CC'.

All of the defaults in 2020 were from emerging and frontier market sovereigns. By region, Latin America had the most defaults, with five, from Argentina, Belize, Ecuador, and Suriname (which defaulted twice). The other two defaulters, Lebanon and Zambia, were from the Middle East and Africa region.

All but one of these sovereign defaults resulted to some extent from the unprecedented credit challenges of COVID-19 and the oil price collapse. Both Ecuador and Suriname grappled with economic shocks as falling oil prices hit exports. This led Ecuador to delay payment on a number of global bonds in April after reaching agreements with a majority of its respective bondholders. Suriname defaulted twice in 2020: In July it began and completed a distressed debt exchange, and by end-October, the new government proposed a standstill on foreign currency debt service payments.

Meanwhile, Belize faced a sharp economic contraction from the COVID-19 pandemic, and as its tourism industry reeled, the government reached an agreement with bondholders in August to amend the terms on its 2034 bond.

Zambia's access to liquidity and external financing became impaired as investors curtailed their exposure to credit risk in response to the pandemic, and the Zambian government suspended debt service payments to external commercial creditors in October.

In Argentina, the pandemic heightened the fiscal strain of weaker revenue, higher expenditure, and unfavorable conditions in the external financing markets. The sovereign missed payments of local-law U.S. dollar-denominated bonds in April and of foreign-law foreign currency bonds in June.

Only Lebanon's default was unrelated to COVID-19, with the fiscal, external, and political pressures that led to the eventual default preceding COVID-19's impact on the country. Lebanon confirmed its first case of COVID-19 on Feb. 21, 2020, and in an unrelated rating action on the same day, we lowered our long-term foreign currency rating on the country to 'CC' because a distressed exchange or unilateral default was virtually certain.

Charts 2 through 7 show the rating histories of these sovereigns that defaulted in 2020.

https://www.spglobal.com/ratings/en/research/articles/210412-default-transition-and-recovery-2020-annual-sovereign-default-and-rating-transition-study-11888070